Valuing a small business in Ireland is key whether you’re buying, selling, or planning. The process involves understanding the business’s worth through financial data, market comparisons, and specific valuation methods tailored to Irish SMEs. Here’s what you need to know:

- Main Valuation Methods:

- Market-Based: Compares recent sales of similar businesses.

- Earnings-Based: Uses EBITDA and industry-specific multipliers.

- Asset-Based: Focuses on assets minus liabilities, ideal for asset-heavy industries.

- Key Steps:

- Gather accurate financial records (e.g., audited accounts, VAT filings).

- Normalise EBITDA (adjust for one-off costs and align salaries with market rates).

- Compile operational/legal documents (leases, contracts, CRO filings).

- Common Multipliers:

- EBITDA multipliers range from 2x to 7x, depending on profitability and business type.

- Revenue-based valuations may apply for high-growth startups.

- Risks to Address:

- Owner dependency and customer concentration can lower multipliers.

- Strong recurring revenue or proprietary assets can increase value.

- Goodwill and Intangibles:

- Brand strength, loyal customers, and exclusive market positions add to value.

Using Irish market data and professional advisers ensures a realistic valuation. Platforms like Bizmark provide benchmarks and tools for SMEs in Ireland.

Quick Tip: Businesses with well-organised records, diversified client bases, and minimal owner reliance often achieve higher valuations.

Preparing for the Valuation Process

Before diving into any valuation method, it’s crucial to ensure your documentation is accurate and well-organised. Buyers, advisers, and lenders will carefully examine your records, and any inconsistencies or missing information can weaken your position and lower your asking price. Getting your documents in order early can make negotiations smoother and more favourable. Start by focusing on your financial records.

Collecting Financial Records

Accurate financial data is the backbone of any valuation. At the very least, you’ll need the following:

- Three years of audited or certified financial statements

- Recent management accounts

- Tax returns filed with Revenue

- VAT records

It’s also important to normalise your EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortisation). This involves adjusting for one-off costs like legal fees from previous restructurings and aligning owner salaries with market rates. For instance, if a working director is earning €120,000 annually but the market rate for that role is €65,000, you should adjust the figures accordingly to reflect what a new owner would realistically pay.

Compiling Operational and Legal Information

Financial data alone doesn’t paint the full picture. Buyers will want to see operational and legal documents as well. Key items to gather include:

- Leases

- Supplier contracts

- Customer agreements

- Long-term service contracts

These documents help buyers assess risk. A business backed by multi-year contracts with key clients is often more appealing than one dependent on informal or short-term arrangements. Also, make sure your Companies Registration Office (CRO) filings are up to date and address any outstanding Revenue compliance issues before entering the market. Deloitte Ireland highlights the importance of resolving these matters early:

"Any matters that will detract from value are likely to come to light as part of any due diligence, so advance knowledge of the issues serves to manage expectations around price when entering negotiations."

If your business has a shareholder agreement, it’s worth reviewing it carefully. As Irish Business Valuations explains:

"Shareholder agreements often stipulate how the business or a shareholding therein must be valued in certain circumstances."

Once you’ve gathered your financial and legal documents, seeking expert advice can help you navigate the next steps.

Working with Professional Advisers and Platforms

An experienced Irish accountant or tax adviser brings an impartial perspective that business owners often lack. These professionals can help normalise your financials, compare your business to similar transactions in Ireland, and produce a valuation that holds up to scrutiny from both buyers and Revenue.

Additionally, platforms like Bizmark can complement this process. They offer indicative valuations, benchmark your business against live Irish market data, and connect you with vetted buyers actively looking for SMEs in your sector. Whether you’re preparing to sell or just want to understand your business’s current value, combining professional expertise with the right platform gives you the clearest and most credible valuation.

sbb-itb-755c06c

Key Valuation Methods for Irish SMEs

Irish SME Valuation Methods: Key Metrics & EBITDA Multipliers Compared

Once your documents are organised and advisers are on board, the next step is figuring out your business’s value. In Ireland, valuers often rely on two or more methods to cross-check results for accuracy. Below, we break down the key valuation methods and how they are applied to Irish SMEs.

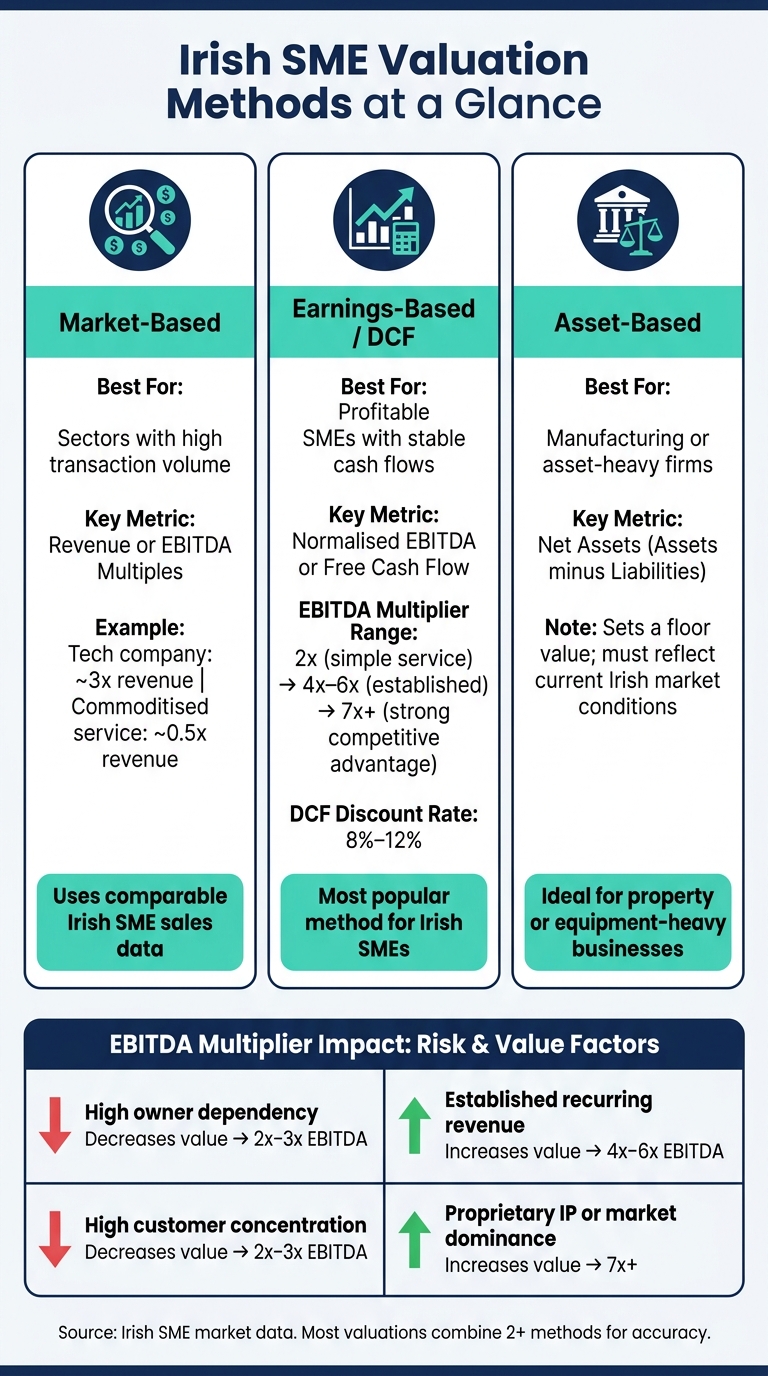

Market-Based Valuation

This approach compares recent sales data from similar businesses. The idea is to use comparable transactions to establish typical revenue or EBITDA multiples, adjusted to reflect your business’s unique characteristics.

For example, a tech company in Ireland might achieve a multiple of around 3x revenue, while a service business in a more commoditised sector might only reach 0.5x revenue. Tools like Bizmark are particularly useful here, offering live benchmarks based on actual Irish SME listings and sales data.

"A valuation in advance of a sales process can be beneficial to the owner in setting a realistic expectation of the sales price the business could achieve in the market." – Linda Melady, Director, Deloitte Ireland

Earnings and Cash Flow Valuation

This method is highly popular for profitable Irish SMEs. It involves applying an industry-specific multiple to normalised EBITDA. Multiples in Ireland generally range from 2x for simpler service businesses to 7x or higher for companies with strong competitive advantages or proprietary assets. Most established businesses tend to fall within the 4x to 6x range. Sales are commonly structured on a debt-free, cash-free basis, making EBITDA the key profitability measure.

For businesses with fluctuating cash flows, a Discounted Cash Flow (DCF) analysis may be more appropriate. DCF calculates the present value of projected future earnings, using a discount rate – typically between 8% and 12% in Ireland – to factor in inflation and risk. This method captures growth potential that a straightforward EBITDA multiple might miss.

Asset-Based Valuation

Asset-based valuation determines a business’s value by subtracting total liabilities from total assets. This method is particularly suited to asset-heavy businesses, such as manufacturing companies or property-holding firms, where the value lies in the assets rather than earnings.

It’s also often used to establish a floor value. Even if a business has a weak trading history, its net assets provide a baseline value below which a seller is unlikely to go. However, it’s crucial that asset valuations reflect current Irish market conditions, not outdated book values. For instance, machinery recorded at €20,000 on the books might have a very different value in today’s market, and relying on stale figures can distort results.

| Method | Best For | Metric |

|---|---|---|

| Market-Based | Sectors with high transaction volume | Revenue or EBITDA multiples |

| Earnings / DCF | Profitable SMEs with stable cash flows | Normalised EBITDA or Free Cash Flow |

| Asset-Based | Manufacturing or asset-heavy firms | Net assets (Assets minus Liabilities) |

Applying Valuation Methods to Irish SMEs

Choosing the Right Valuation Method

When valuing an Irish SME, selecting the right method depends heavily on the sector, profitability, and context of the sale. This builds on the earlier discussions of market, earnings, and asset-based approaches, with adjustments to reflect the specific traits of Irish businesses.

For well-established service firms in Ireland – like legal, accountancy, or recruitment practices – an earnings-based approach using a normalised EBITDA multiplier is often the most suitable. In contrast, asset-based valuations work better for businesses with significant physical assets. For early-stage tech companies or SaaS firms that may not yet be profitable but show strong user growth, methods like times-revenue or a discounted cash flow (DCF) model are better suited to capture their growth potential.

Another useful benchmark is the cost a competitor would incur to replicate your business from scratch. If your earnings-based valuation exceeds this figure, the difference must be justified by genuine goodwill – such as brand recognition, loyal customers, or proprietary systems. If not, the valuation may need to be adjusted downward.

"A valuation differs from a selling price. It provides a starting point for negotiations, but the final price depends on market demand, competition, and timing." – Lena Hanna, CPA

After selecting the valuation method, it’s important to tailor it to account for specific risks that are unique to SMEs.

Adjusting for SME-Specific Risk Factors

Certain risks, like owner dependency or customer concentration, can significantly impact a business’s valuation. These factors act as modifiers to the base valuation and often influence the EBITDA multiplier.

For example, owner dependency – where the business relies heavily on the owner’s relationships or expertise – poses an operational risk for buyers. This typically reduces the multiplier to around 2x–3x EBITDA. On the other hand, businesses with strong management teams, well-documented processes, and recurring revenue streams can command higher multipliers, ranging from 4x to 6x or even more.

Another common issue is customer concentration, where losing a key client could severely impact revenue. Addressing this risk before entering the market, even by diversifying modestly, can improve the final valuation.

| Risk / Value Factor | Effect on Multiplier | Typical Range |

|---|---|---|

| High owner dependency | Decreases value | 2x – 3x |

| High customer concentration | Decreases value | 2x – 3x |

| Established recurring revenue | Increases value | 4x – 6x |

| Proprietary IP or market dominance | Increases value | 7x+ |

Taking these risks into account ensures a more accurate valuation, but it’s equally important to evaluate the intangible assets that can enhance the business’s appeal.

Accounting for Goodwill and Intangible Value

Goodwill is the premium a buyer is willing to pay over a business’s net asset value, and it directly influences the earnings multiplier. Factors like a strong brand, loyal customers, and robust operational systems all contribute to higher goodwill.

Intangible value often stems from assets such as long-term customer contracts, exclusive local market positions, intellectual property, or trademarks. A capable management team that can operate the business independently also adds considerable value. These intangibles make a business more defensible during negotiations compared to one overly reliant on the owner’s personal network.

"Professional business valuers firstly gain a thorough understanding of the target business and then leverage this knowledge with understanding the key value drivers… to determine market valuation metrics." – Stephen O’Flaherty, Partner, Corporate Finance, BDO

For SaaS or subscription-based businesses in Ireland, buyers are increasingly focused on how "sticky" the customer base is. As Grit Young, Partner at EY Ireland, notes: "If evidence comes to light that customers can switch easily, the valuation approach and the comparable/similar business list drawn up by the buyer is called fundamentally into question." This highlights the importance of substantiating intangible value with real evidence rather than assumptions.

Using Irish Market Data and Tools to Refine Your Valuation

Using Market and Financial Benchmarks

Once you’ve accounted for goodwill and intangible assets, it’s crucial to ground your valuation in accurate market data. Without aligning your figures to comparable transactions or sector benchmarks relevant to Ireland, your valuation may falter during negotiations.

A good place to begin is the Companies Registration Office (CRO). Many Irish businesses are required to file annual accounts, giving you access to essential financial data like revenue, profit margins, and balance sheets for companies in your sector. This allows you to create a clear financial profile of similar Irish SMEs, rather than relying on rough estimates.

As Linda Melady, Director at Deloitte Ireland, explains: "An acquirer will focus on EBITDA (Earnings before interest, tax, depreciation and amortisation) as a benchmark for profitability for the business and will typically base the price on a multiple of this metric.". By comparing your normalised EBITDA against sector-specific multipliers, you can build a valuation that’s both credible and defensible.

Platforms like Bizmark also offer valuable market insights. You can browse active listings of Irish SMEs in your sector, providing a realistic view of asking prices and revenue ranges for businesses of a similar size. This is especially useful for valuations in the €5,000–€200,000 range, where detailed transaction data can be harder to find.

Here’s a summary of the key benchmarks by valuation method to guide your comparisons:

| Valuation Method | Best Use Case | Key Benchmark |

|---|---|---|

| Earnings-Based | Profitable service businesses | 2x–7x+ multiplier of normalised EBITDA |

| Times-Revenue | High-growth or pre-profit startups | 0.5x–2x of annual sales |

| Asset-Based | Manufacturing or real estate | Net book value (assets minus liabilities) |

| Entry-Cost | Niche or early-stage businesses | Cost to replicate staff, equipment, and customer base |

Once you’ve established these benchmarks, document your assumptions and rigorously test them to ensure your valuation holds up under scrutiny.

Documenting and Stress-Testing Your Valuation

After comparing your figures against market data, it’s essential to clearly document your valuation assumptions. Create a detailed valuation summary that outlines your chosen method, the multiplier applied, your normalised EBITDA, and the reasoning behind each decision. This summary will serve as your foundation during discussions with potential buyers or advisers in the Irish SME market.

Next, stress-test your valuation by running a couple of scenarios. Start with a base case reflecting current performance, then explore a downside case – for example, a scenario where you lose a key client or experience slower revenue growth. If you’re using a DCF model, consider increasing the discount rate to account for specific Irish market risks, such as sector volatility or rising interest rates. A valuation that remains credible under these stress tests will carry much more weight than one based solely on optimistic projections.

You can also apply the entry-cost method as a reality check. Estimate what it would cost a buyer to replicate your business in Ireland today – factoring in the recruitment of staff, purchase of equipment, and development of a customer base. If your earnings-based valuation is significantly higher than this figure, be ready to back up the difference with solid evidence, such as goodwill or a clear competitive edge.

Conclusion: Key Takeaways for Valuing an Irish SME

Valuing an Irish SME involves balancing financial data, market insights, and practical judgement. The most dependable valuations often combine at least two methods, normalise EBITDA, and take into account specific local factors like market share, owner dependency, and customer concentration unique to Ireland.

Preparation plays a crucial role. Businesses with up-to-date financial records, a broad client base, and clearly documented intangible assets are better positioned to justify their asking price and close deals more efficiently. As Irish Business Valuations notes: "Understanding the true market value of your business before you start a sale process will help secure a successful outcome." These preparatory steps lay the groundwork for a solid and defensible valuation.

A key point to remember is that businesses operating independently of their owners tend to achieve higher valuation multiples. Establishing strong operational systems well in advance of a sale not only reduces risks but also boosts the business’s overall appeal. As mentioned earlier, minimising owner reliance is a practical way to enhance value. In high-stakes situations like a sale, a shareholder dispute, or a tax-related event, engaging an independent professional valuer can be a game-changer. Their impartial assessment strengthens your position during negotiations and ensures the valuation aligns with actual market conditions.

By focusing on thorough preparation, selecting the right valuation methods, and seeking objective expertise, you can confidently determine your SME’s market value.

Bizmark caters specifically to the Irish SME sector, targeting businesses valued between €5,000 and €200,000. Whether you’re selling or researching comparable businesses, Bizmark provides direct access to authentic Irish market data – no guesswork required.

FAQs

Which valuation method suits my business best?

The best way to value a business depends on its type and your specific goals. For service businesses that are already profitable, an earnings-based valuation using an industry-specific multiplier is often a solid choice. On the other hand, startups with rapid growth might lean towards a times-revenue method. If your business is asset-heavy, such as in manufacturing or real estate, a book valuation often proves more effective. For critical decisions like selling your business or securing investment, it’s worth seeking advice from a professional.

How do I normalise EBITDA for a sale in Ireland?

When preparing a business for sale in Ireland, normalising EBITDA is a key step. It involves adjusting the earnings to exclude any non-recurring, irregular, or owner-specific expenses and revenues. The goal here is to ensure EBITDA accurately reflects the business’s ongoing operational performance.

Some common adjustments include:

- Removing owner-specific expenses, such as personal travel or non-business-related costs.

- Excluding non-recurring costs or income, like one-off legal fees or exceptional gains.

- Adjusting for related-party transactions that may not occur under new ownership.

The result? A normalised EBITDA that provides a clearer picture of the business’s sustainable profitability. This clearer view is essential for determining an accurate valuation and presenting the business in its best light to potential buyers.

What documents will buyers ask for during due diligence?

During the due diligence process, buyers usually ask for specific documents to assess a business’s value, financial position, and legal compliance. These often include:

- Financial records: Such as profit and loss accounts, balance sheets, and cash flow statements.

- Tax documentation: Including past filings and records.

- Asset information: Registers and ownership certificates for physical or intangible assets.

- Valuation reports: Documents detailing the business’s estimated worth.

- Legal paperwork: Incorporation documents, shareholder agreements, and contracts.

These materials are essential for verifying the business’s claims and identifying any potential risks.